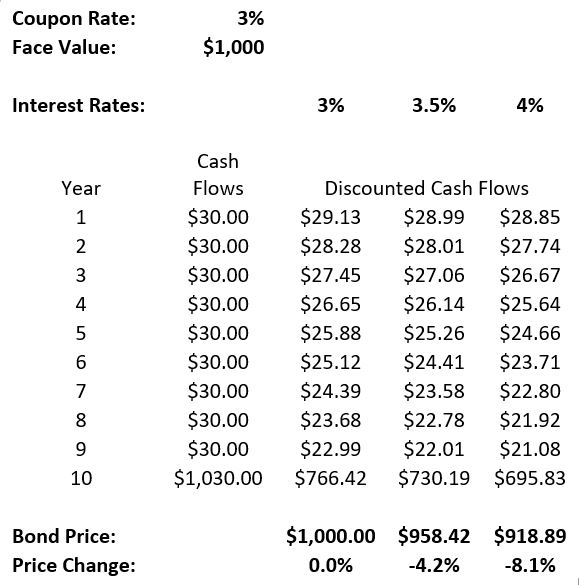

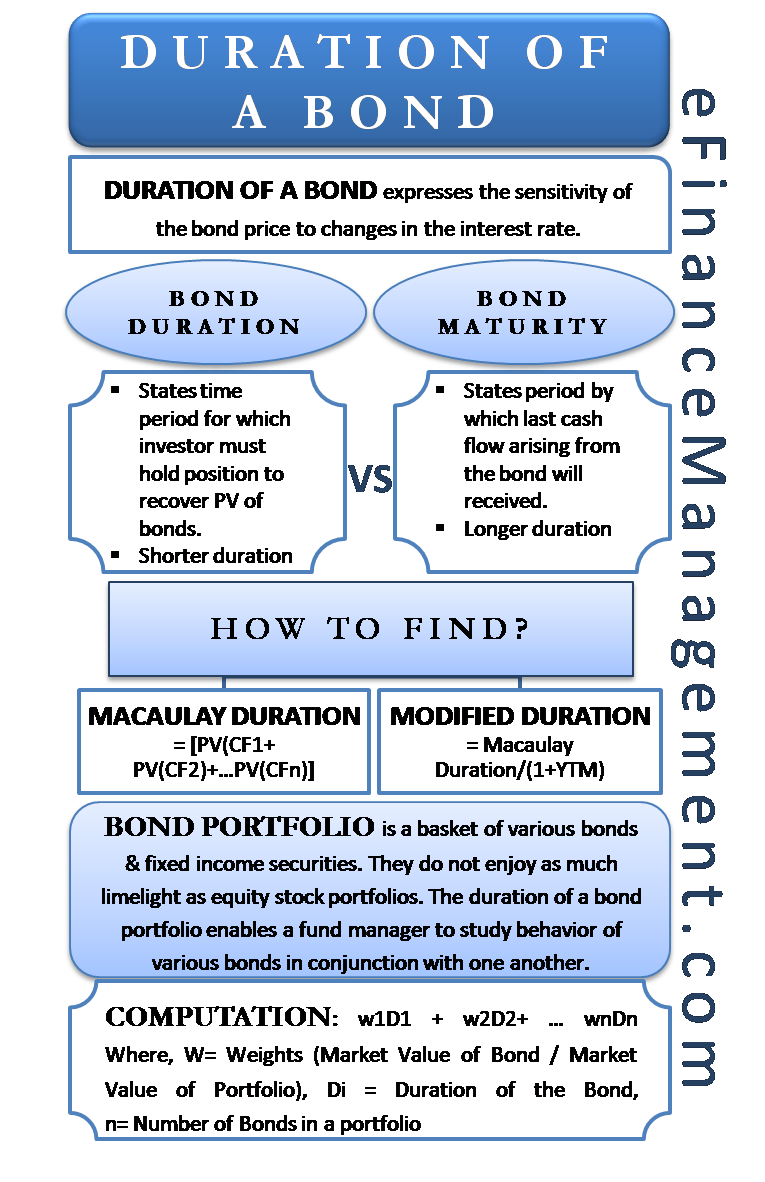

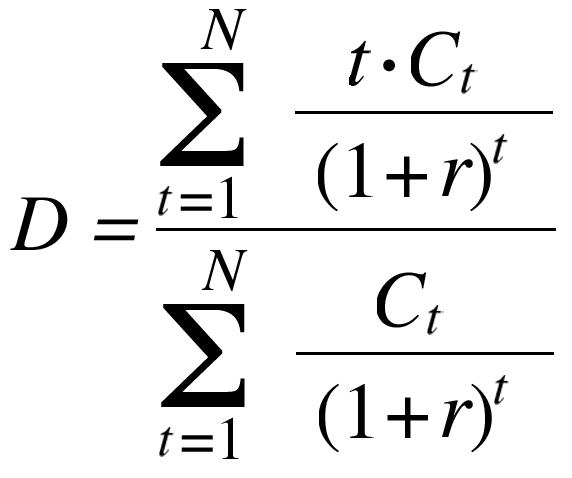

42 duration of a coupon bond

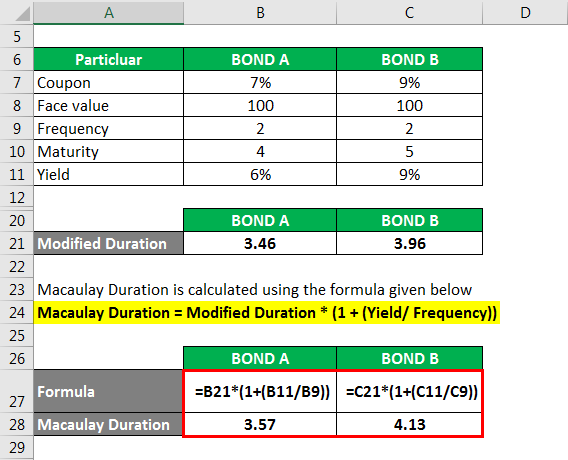

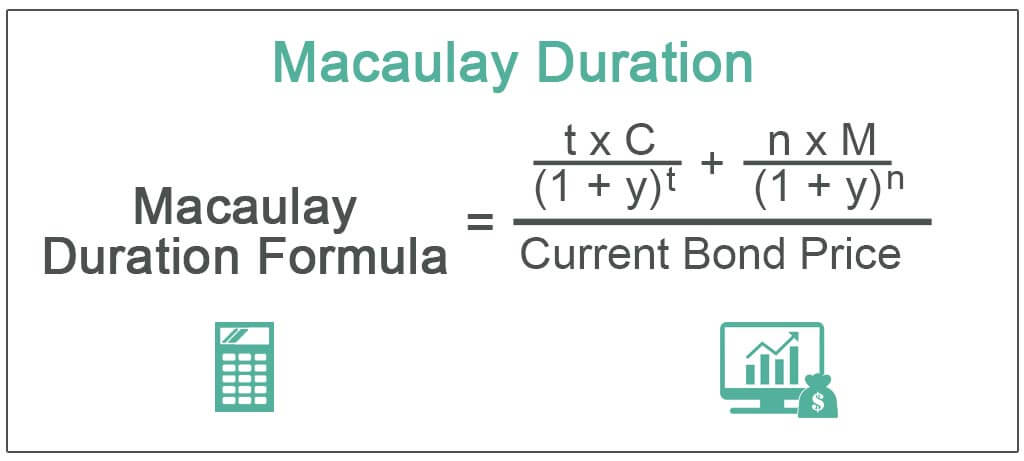

› macaulay-duration-formulaMacaulay Duration Formula | Example with Excel Template - EDUCBA Using the above formula, Macaulay Duration of Bond A is at 3.57 while Macaulay Duration of Bond B is at 4.13. Macaulay Duration Formula – Example #2. Let us take another example and calculate Macaulay Duration using the longer method. Let us take a Bond A $100 value bond that pays a 6% coupon rate and matures in four years. › terms › dDuration Definition and Its Use in Fixed Income Investing Sep 01, 2022 · Duration is a measure of the sensitivity of the price -- the value of principal -- of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Bond ...

› fixed-income-bonds › durationDuration: Understanding the relationship between bond prices ... That said, the maturity date of a bond is one of the key components in figuring duration, as is the bond's coupon rate. In the case of a zero-coupon bond, the bond's remaining time to its maturity date is equal to its duration. When a coupon is added to the bond, however, the bond's duration number will always be less than the maturity date.

Duration of a coupon bond

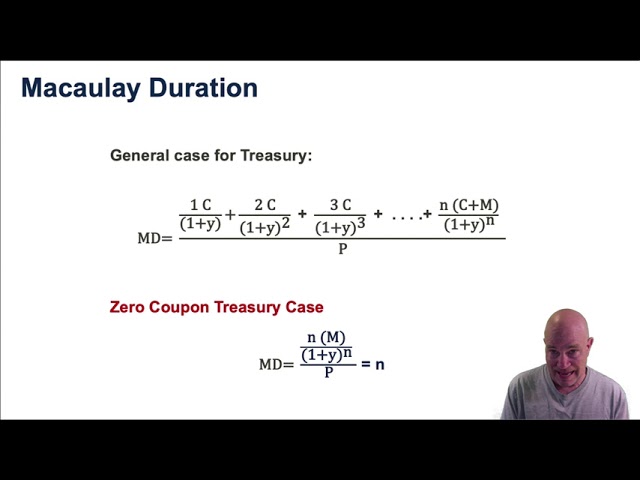

en.wikipedia.org › wiki › Bond_durationBond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond. Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield. › ask › answersBond Coupon Interest Rate: How It Affects Price - Investopedia Dec 18, 2021 · A bond's current yield, however, is different: a percentage based on the coupon payment divided by the bond's price, it represents the bond's effective return. Coupon Interest Rate vs. Yield dqydj.com › bond-duration-calculatorBond Duration Calculator – Macaulay and Modified Duration From the series, you can see that a zero coupon bond has a duration equal to it's time to maturity – it only pays out at maturity. Example: Compute the Macaulay Duration for a Bond. Let's compute the Macaulay duration for a bond with the following stats: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5% ...

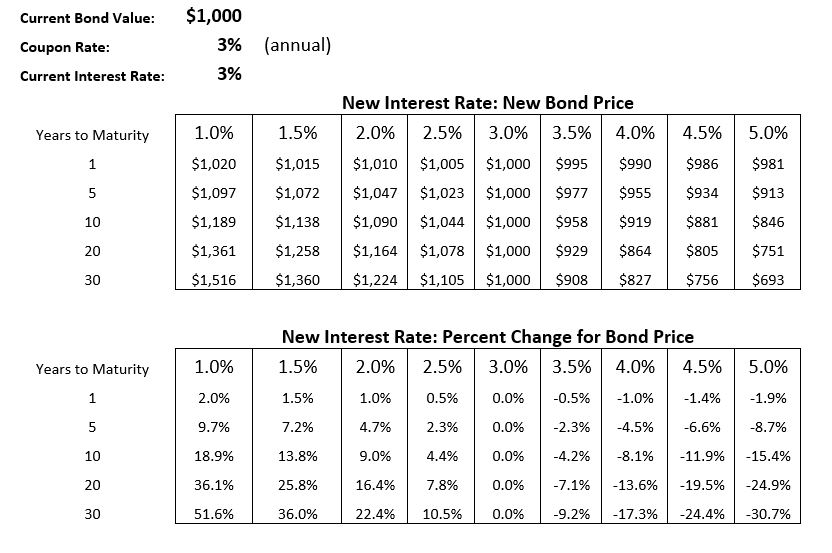

Duration of a coupon bond. calculator.academy › zero-coupon-bond-calculatorZero Coupon Bond Calculator - Calculator Academy Oct 28, 2022 · To calculate a zero coupon bond value, divide the face value by 1 plus the rate raised to the power of the time to maturity. Zero Coupon Bond Definition A zero-coupon bond is a security that does not pay interest but trades at a discount and renders a profit at maturity when the bond is redeemed for its face value. dqydj.com › bond-duration-calculatorBond Duration Calculator – Macaulay and Modified Duration From the series, you can see that a zero coupon bond has a duration equal to it's time to maturity – it only pays out at maturity. Example: Compute the Macaulay Duration for a Bond. Let's compute the Macaulay duration for a bond with the following stats: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5% ... › ask › answersBond Coupon Interest Rate: How It Affects Price - Investopedia Dec 18, 2021 · A bond's current yield, however, is different: a percentage based on the coupon payment divided by the bond's price, it represents the bond's effective return. Coupon Interest Rate vs. Yield en.wikipedia.org › wiki › Bond_durationBond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond. Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield.

Solved An 8% coupon bond with 20 years to maturity selling ...

Bond Duration - Retirement Researcher

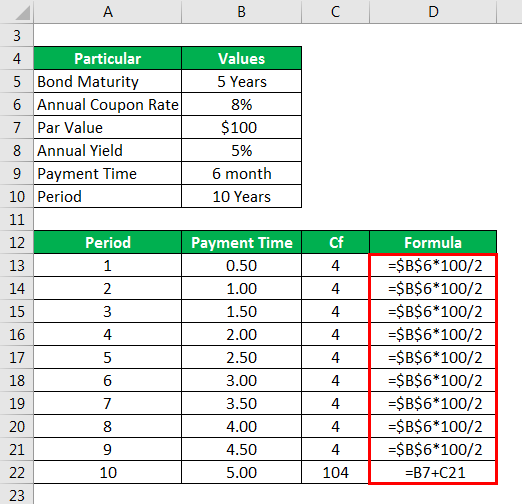

Calculation of Duration and Convexity (5-year, $100 face ...

4 Measuring Interest-Rate Risk: Duration

Solved] Consider a three-year maturity, 8 percent annual ...

Bond Price Volatility Zvi Wiener Based on Chapter 4 in ...

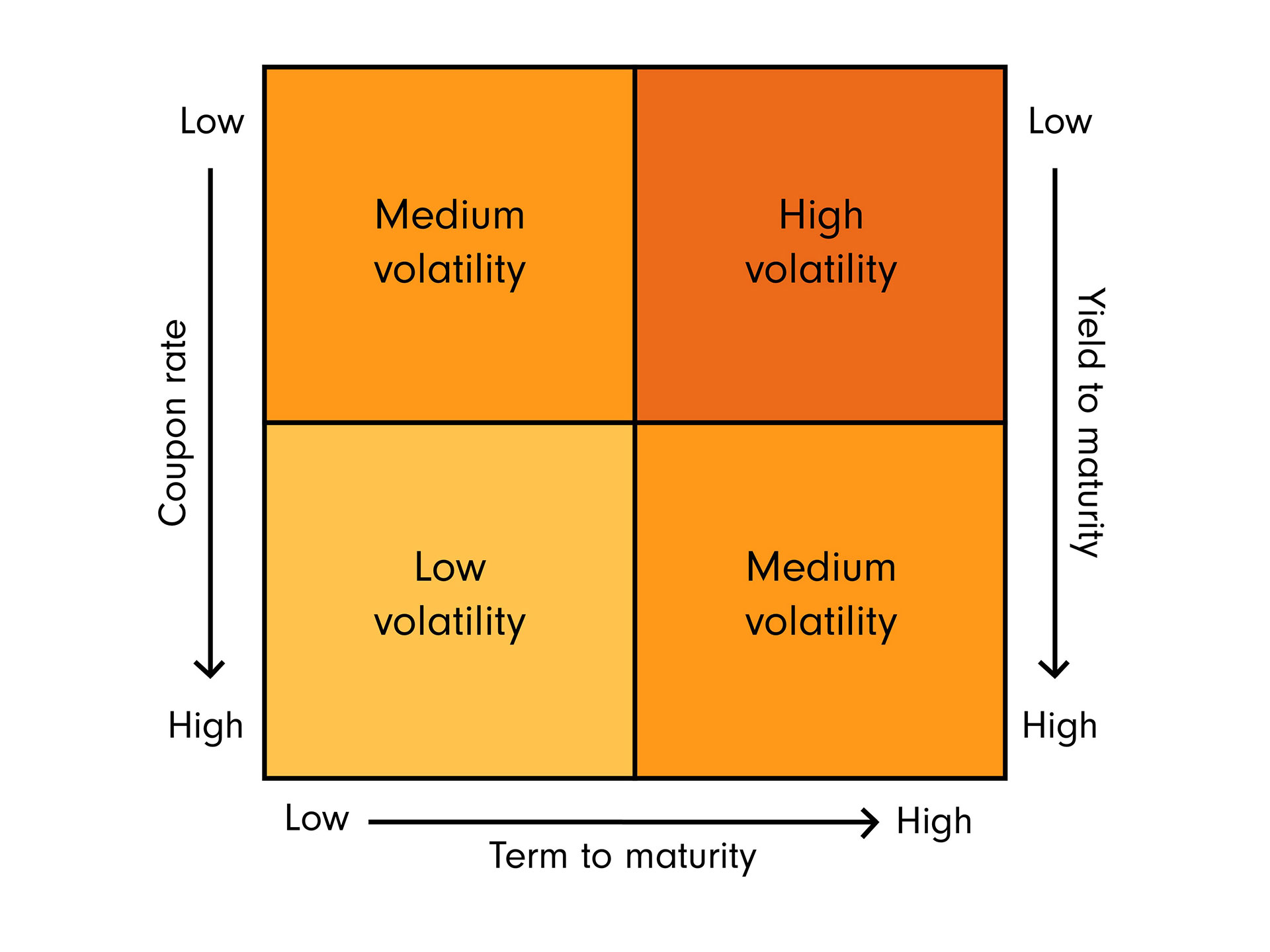

THE RELATIONSHIP BETWEEN YIELD DURATION AND MATURITY

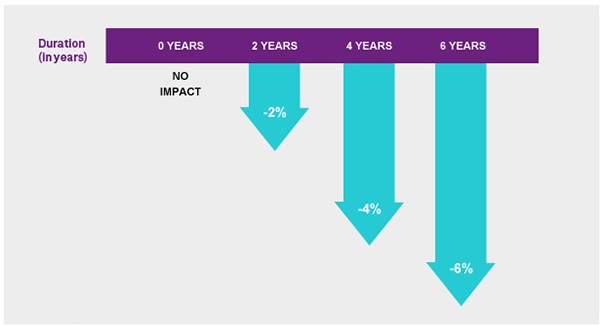

Making sense of duration sensitivity | Fidelity Singapore

Macaulay Duration Definition & Example | InvestingAnswers

Measures of Price Sensitivity 1

Bond Portfolio Duration and the Flaw of Averages | Morningstar

FRM: Dollar duration of zero coupon bond

Zero-Coupon Bonds: Characteristics and Examples

Zero Coupon Bond Value - Formula (with Calculator)

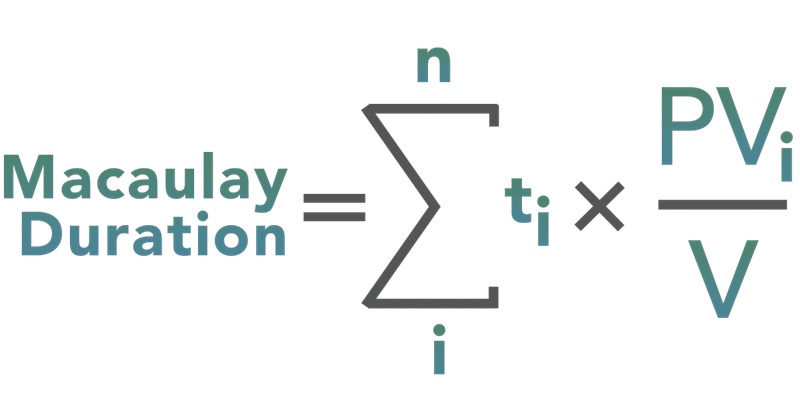

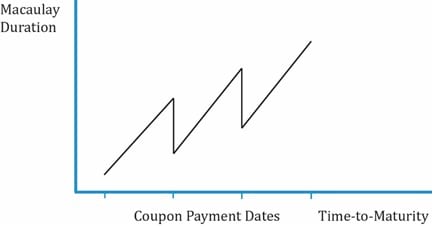

Macaulay Duration

Bond Duration - Retirement Researcher

Duration and Zero Coupon Bonds - YouTube

DOC) Chapter 16 Managing Bond Portfolios Multiple Choice ...

Modified duration of zero-coupond bond (FRM practice question)

Under the Hood: What You Need to Know About Bond Duration and ...

Macaulay Duration Formula | Example with Excel Template

Duration and Convexity in Bond market

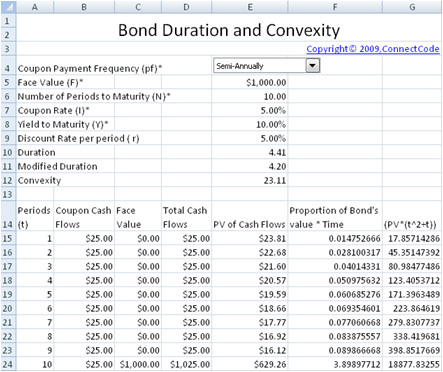

Free Bond Duration and Convexity Spreadsheet

Understanding bond duration - Education | BlackRock

Understanding Fixed-Income Risk and Return | IFT World

Premium Bonds 101 | Breckinridge Capital Advisors

Bond Modified Duration in R | R-bloggers

Macaulay Duration of a Semi annual coupon bond

Aha! Interest rates do matter.

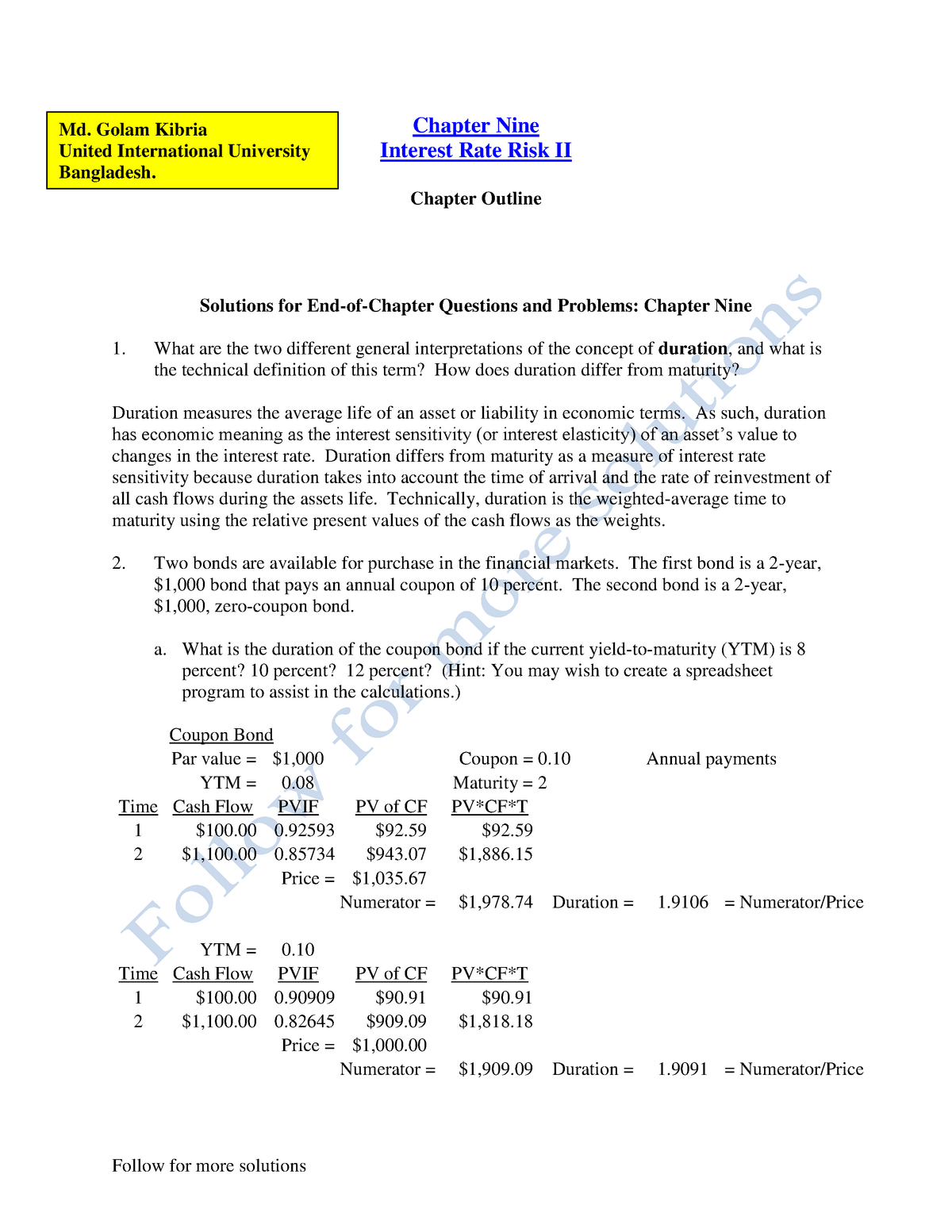

Chap009 duration gap model - Md. Golam Kibria United ...

Macaulay, Modified, and Effective Durations | CFA Program ...

Duration and Convexity, with Illustrations and Formulas

Modified Duration - Zero Coupon Bond Modified Duration ...

Bond's Maturity, Coupon, and Yield Level | CFA Level 1 ...

Modified Duration | Explanation, Example with Excel Template

Solved] Find the duration of a 6% coupon bond making annual ...

Duration & Convexity - Fixed Income Bond Basics | Raymond James

Define Duration

Duration of a Bond | Portfolio Duration | Macaulay & Modified ...

Investment Improvement: Adding Duration to the Toolbox | St ...

Duration: a measure of bond price volatility | Nuveen

Macaulay Duration (Definition, Formula) | Calculation with ...

Post a Comment for "42 duration of a coupon bond"